Outlook 2022: Rates – Upward Pressure

- 16 December 2021 (5 min read)

Key points

- The effect of interest rate and inflation expectations on 10-year US Treasury yields has been rather modest in 2021, as the Federal Reserve remains in control of market volatility and the term premium

- However, inflation dynamics could – if proven more structural – accelerate the process of monetary policy normalisation, with consequences not only for government bond markets, but also for riskier asset classes and currencies

- Overall, our analysis suggests that several factors might contribute to higher Treasury yields over the course of 2022.

The last line of defence: The term premium

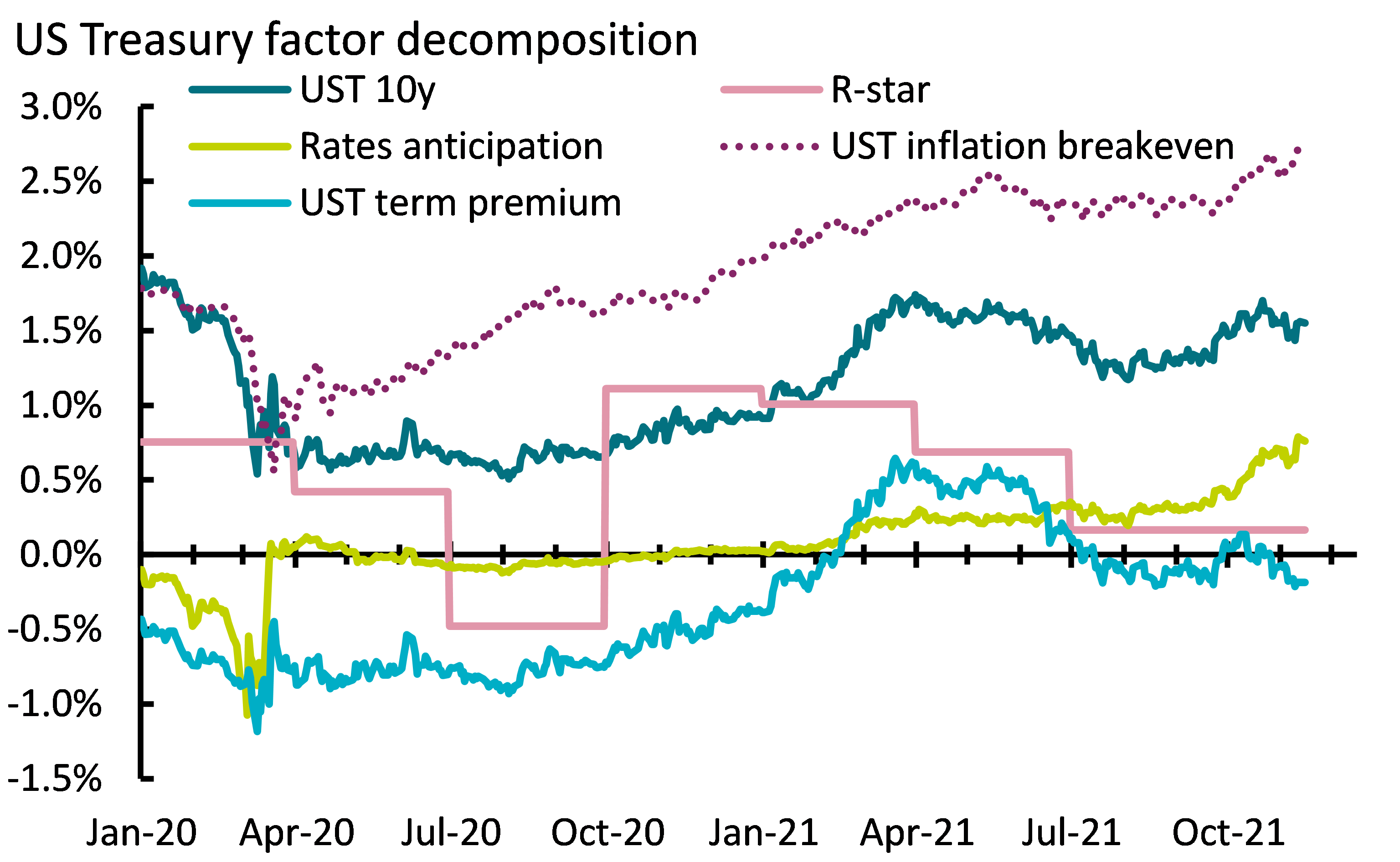

During 2021 we have seen a positive contribution to US Treasury yields both from interest rate and inflation expectations, while the term premium is only marginally higher. Exhibit 1 shows the 75 basis-point rise in both 10-year breakevens and Federal Reserve (Fed) rate expectations. Ex-post, the real equilibrium rate (R-star, which cannot be observed directly) may also have risen somewhat, reflecting productivity-augmenting public investments. As a result, US Treasuries have delivered a -2.9% performance year-to-date, against a 6.2% return for the Treasury Inflation-Protected Security index.

Exhibit 1: Factors driving Treasury yields

Source: Bloomberg and AXA IM Research, 15 November 2021

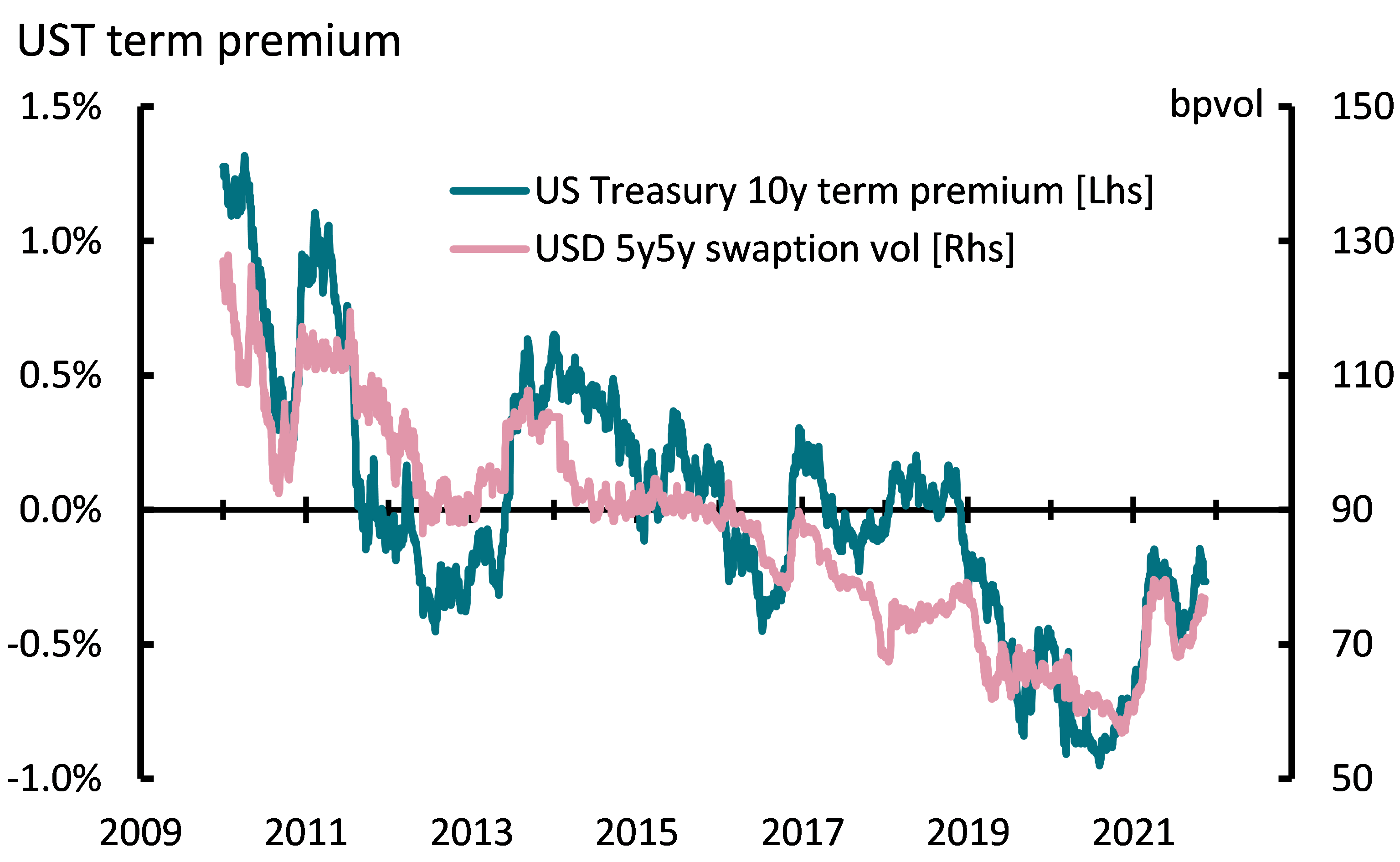

The term premium merits our special attention, not least because of its sensitivity to unconventional monetary policy. Market participants have long shared the view that the Fed might be the largest seller of volatility in the world. In our view, this is the longer-term function of quantitative easing (QE), equivalent to saying that the Fed is implicitly conducting a form of yield curve control by preventing the term premium from reflating back to its historical averages. The relationship between US dollar swap option implied volatility and the Treasury term premium (Exhibit 2) provides us with an empirical validation of the theoretical foundations of bond risk premia. It is reasonable to expect the Fed to conduct a smooth tapering in order to avoid a quick normalisation of market volatility and hence of term premia across the curve.

Exhibit 2: The relationship between volatility and yields

Source: Bloomberg and AXA IM Research, 15 November 2021

Global QE: One step closer to the cliff

The process of tapering is by no means unique to the Fed, as all systemic central banks – except the Bank of Japan – are currently discussing their own form of transitioning to a lesser QE world. The unprecedented level of synchronisation between macroprudential, monetary and fiscal policies has had its effect on the size of central banks’ balance sheets (Exhibit 3). In contrast to the policy mix put in place in response to the global financial crisis, the strategies implemented to cope with COVID-19 have been designed to partially bypass the banking sector in reaching out to the real economy, thus reaching firms and households directly with more direct consequences on inflation.

Exhibit 3: Unprecedented policy co-ordination

Source: Bloomberg and AXA IM Research, 15 November 2021

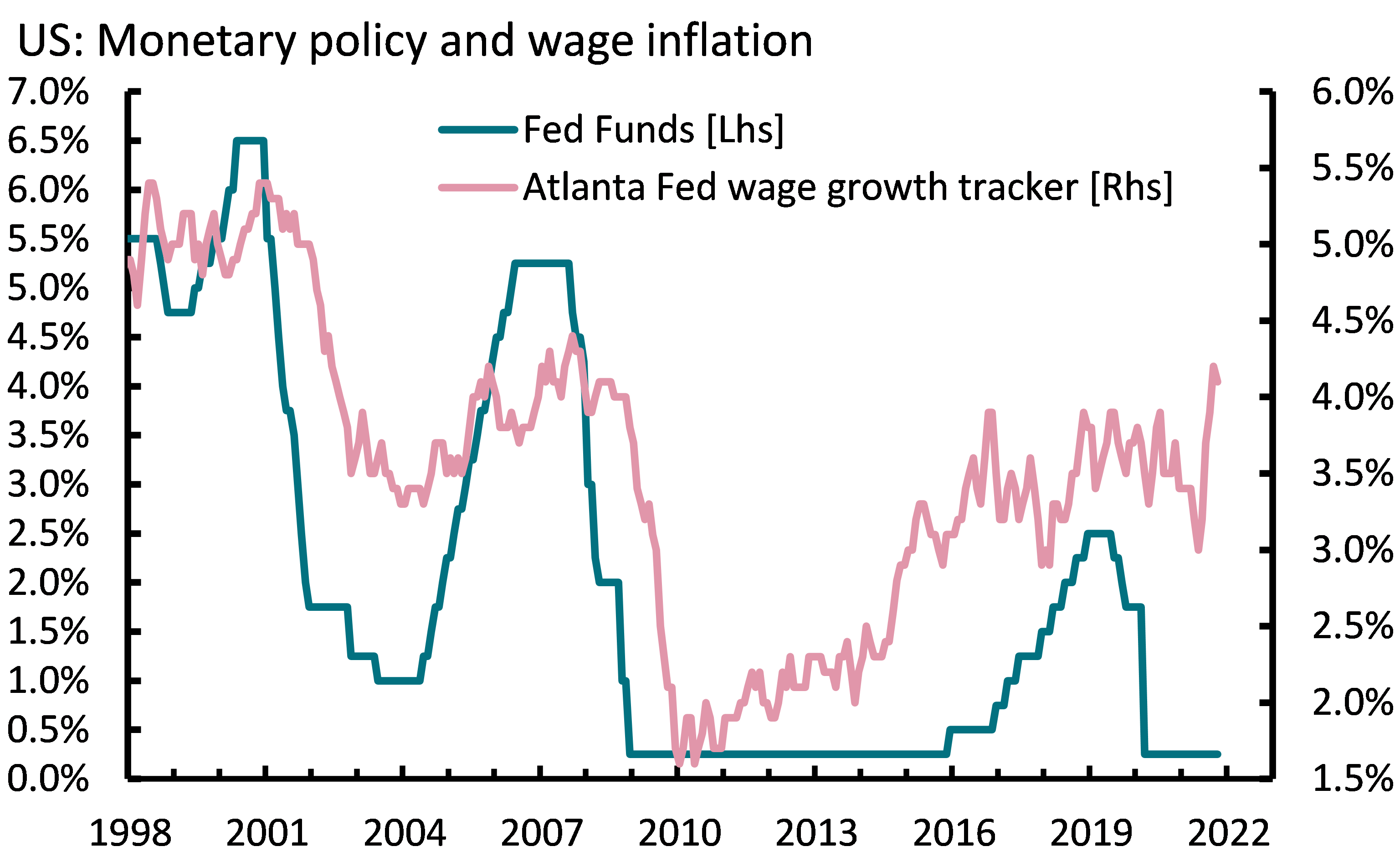

Without entering into a lengthy discussion on the various drivers of inflation, we stress that the contribution of wages to overall price pressure has been modest so far. Of course, surveys suggest that wage pressure is building rapidly in some regions and might pass through the price pipeline. Central banks might have to hike rates as soon as policy normalisation criteria are met, thus narrowing the gap between wages and policy rates (Exhibit 4). The risk is that the longer they appear to fall behind the inflation curve, as now explicitly required by some policy strategies, the faster they might have to unwind accommodative policy stances.

Exhibit 4: Wage pressure mounting

Source: Bloomberg and AXA IM Research, 15 November 2021

The changing structure of the European government bonds market

It is not unreasonable to believe that unconventional monetary policy may at times distort bond markets’ price signalling function, given the size of central banks’ balance sheets relative to the economy. The effect of QE on the bond markets can also be seen in the Eurozone, where the combination of the European Central Bank’s (ECB) Public Sector Purchase Programme and the Pandemic Emergency Purchase Programme has extracted something like 55% of the government bond market’s duration risk (Exhibit 5).

Exhibit 5: Duration extraction going too far?

Source: ECB, IHS Markit and AXA IM Research, 15 November 2021

Unfortunately, the ECB balance sheet’s extraordinary size might introduce a new breed of risks linked to liquidity into euro government bond markets. Therefore, we cannot rule out more frequent collateral scarcity episodes in the months to come, which could require the ECB to intervene on repo markets, as is often the case going into year-end. These events are partly also related to the interplay between the primary market and investors’ risk management needs.

Putting the pieces together

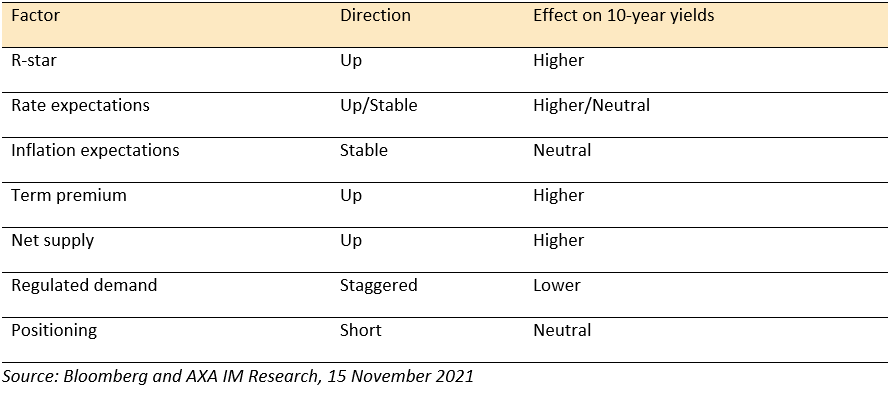

To conclude our brief overview and outlook of the rates space, we list the main factors determining our view for the direction of Treasury yields (Exhibit 6): Given the current market and macro setup, Treasury yields are more likely to rise than to fall within a medium-term horizon.

Exhibit 6: Qualitative Treasury yield scorecard

We conclude with three additional observations:

- The absolute yield level matters for regulated bond demand, i.e. flows originating from compliance with financial regulation. One example is the complex relationship between asset/liability valuations and the demand for government bonds by insurance companies. Therefore, we believe that this type of demand is going to be staggered at best and won’t be a permanent force acting upon bond prices.

- The speed at which yields rise also matters for overall risk appetite/aversion. The Fed’s 2013 tapering and the German bund’s 2015 value-at-risk shock are perfect examples of the effect of fast markets on dealers’ ability to warehouse and to process risk. A similar scale variation, albeit spanning over a longer time horizon, might have had only a limited spill-over into other asset classes.

- Almost by definition, lags between central banks will affect cross-market spreads as well as currencies’ valuation and hedging costs. We are already observing a close link between the widening two-year Treasury versus Schatz spread and the declining euro/dollar exchange rate. The precise sequence and timing of central banks lifting off their rates floor is therefore key in understanding and capturing the relative value between international bond markets in 2022.

Disclaimer

This website is published by AXA Investment Managers Asia (Singapore) Ltd (ARBN 115203622) (“AXA IM Asia”). AXA IM Asia is exempt from the requirement to hold an Australian Financial Services License and is regulated by the Monetary Authority of Singapore under Singaporean laws, which differ from Australian laws. AXA IM Asia offers financial services in Australia only to residents who are “wholesale clients" within the meaning of Corporations Act 2001 (Cth).

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk , including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested.

Disclaimer

This website is published by AXA Investment Managers Australia Ltd (ABN 47 107 346 841 AFSL 273320) (“AXA IM Australia”) and is intended only for professional investors, sophisticated investors and wholesale clients as defined in the Corporations Act 2001 (Cth).

This publication is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Market commentary on the website has been prepared for general informational purposes by the authors, who are part of AXA Investment Managers. This market commentary reflects the views of the authors, and statements in it may differ from the views of others in AXA Investment Managers.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk , including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested.