Consumer watch

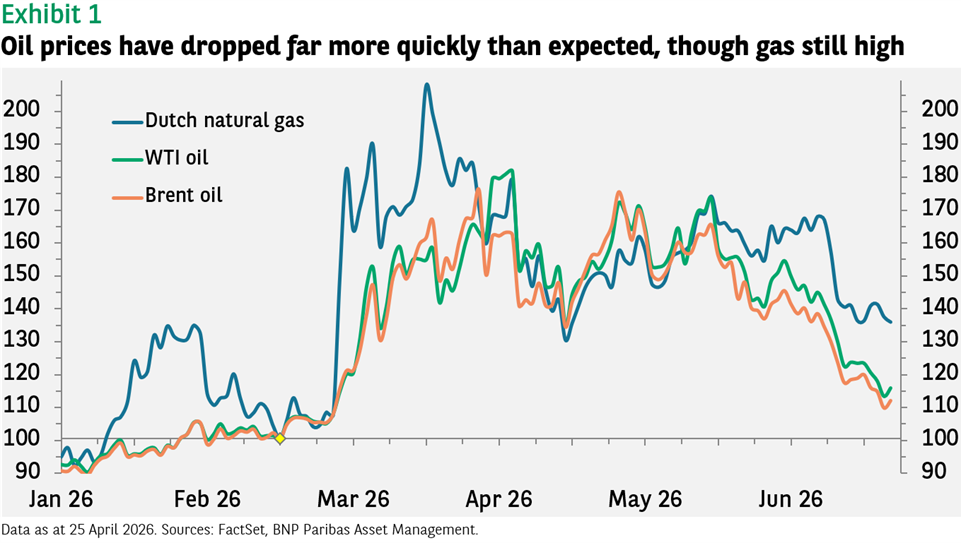

Oil prices dropped far more quickly than many analysts expected following the announcement of the Memorandum of Understanding between the US and Iran.

Despite delays in restoring traffic through the Strait of Hormuz and damage to infrastructure in the Middle East, oil prices have moved back towards pre-war levels, if not quite the lows reached in January. Importantly for Europe, natural gas prices are still elevated (Exhibit 1).

Equity markets have welcomed the geopolitical developments, with non-technology indices such as Russell Value or MSCI Europe gaining 2% to 3% since early June.

This performance stands in contrast to what has happened to tech stocks in the US and emerging markets, where indices have declined by 2% to 4%. The drop is a function of investor worries about excessive exuberance, particularly for Korean stocks, as leveraged ETF bets on further gains suggested markets were getting frothy.

The Nasdaq index has also had to adjust to modestly higher policy rate expectations following the hawkish press conference from the Federal Reserve in mid-June.

Economic data

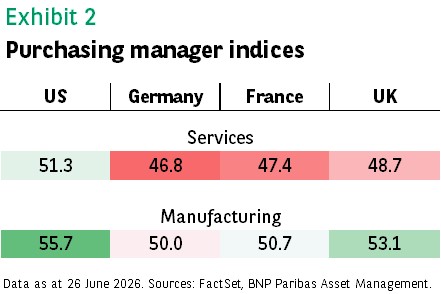

Economic data continues to point to a further acceleration of activity in the US, alongside contraction or sluggish growth in Europe. The US services sector Purchasing Managers’ Index moved further into expansionary territory (a reading above 50), while those for the major economies of Europe were well below.

The US manufacturing PMI hit its highest level in four years (despite, or because of, tariffs), while the figures for continental Europe were more modest (see Exhibit 2). To the degree that higher energy prices would have a bigger impact on manufacturing than on services, Europe’s poor services figures are worrying.

Not all the data for the US is encouraging, however. The final revision to US first quarter GDP raised the figure from 1.6% to 2.1%. Artificial intelligence-driven business investment remains strong, and the offsetting drag to growth from net exports is lower (much of the AI capital expenditure is spent on importing semiconductor chips, which worsens the trade balance).

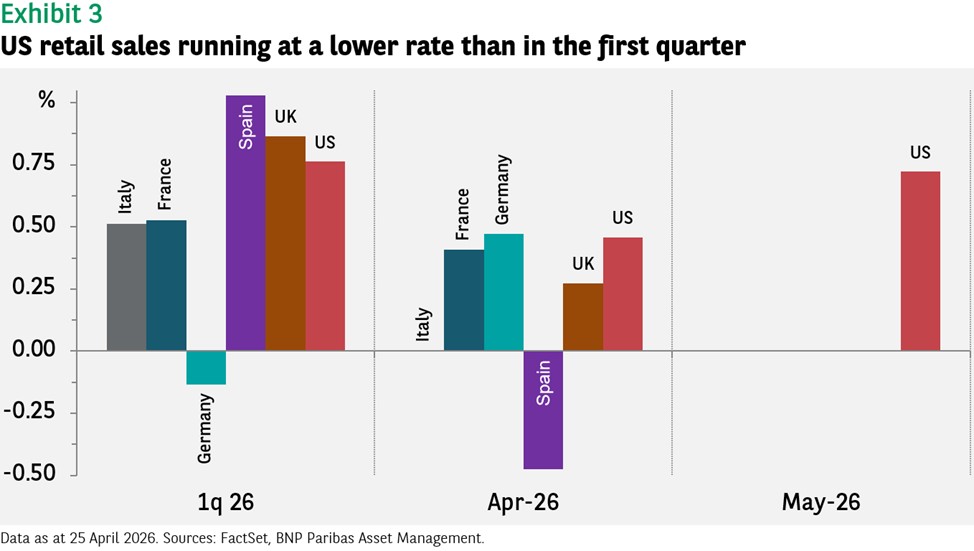

The concerning figure was consumer demand, which was revised down from an already low 1% to 0.4%. The long-run, non-recessionary average for PCE (personal consumption expenditures) is 2%. The data suggests that the US consumer may be struggling.

Anticipating what the PCE figure for the second quarter might turn out to be, US retail sales have been running at an even lower rate, though this is true for most of Europe, too (see Exhibit 3).

With business activity evidently still robust, the consumer remains the key vulnerability to US equity markets.

Data sources: FactSet, BNP Paribas Asset Management as of 25 June 2026 (unless otherwise stated). Past performance should not be seen as a guide to future returns.

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Australia Ltd (ABN 47 107 346 841 AFSL 273320) (“AXA IM Australia”) and is intended only for professional investors, sophisticated investors and wholesale clients as defined in the Corporations Act 2001 (Cth).

This publication is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Market commentary on the website has been prepared for general informational purposes by the authors, who are part of AXA Investment Managers. This market commentary reflects the views of the authors, and statements in it may differ from the views of others in BNP Paribas Asset Management.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk , including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested.