Is it time for short duration inflation-linked bonds?

KEY POINTS

Global bond markets suffered in March as inflation fears created by the Middle East conflict led to a major rise in interest rates.

The upward move was triggered by surging energy prices in the wake of the war, which has all but halted oil and gas flows from the Middle East.

The backdrop has fuelled inflation worries. Should the war drag on, time will play against the global economy and price stability, with a rising risk of stagflation — increasing inflation mixed with stagnant growth.

A combination of low growth and high inflation is a rare and unpleasant experience in developed economies, since a weak economy normally means tepid demand and a fragile labour market, dragging down price rises

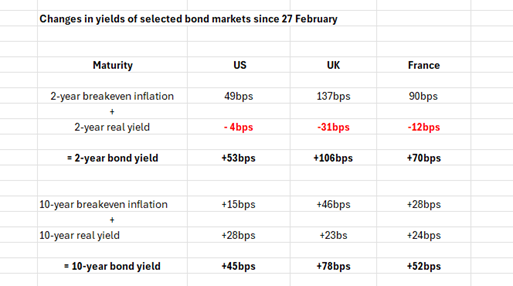

Markets now expect central banks to raise rather than lower interest rates in 2026. As a result, short-term debt bore the brunt of March’s sell-off, as investors abruptly shifted from anticipating central banks interest rate cuts to hikes to counter higher inflation. Exhibit 1 shows the changes in selected bond yields in the US, eurozone and UK in March.

Exhibit 1: Changes in yields of selected bond markets since 27 February

Source: BNPP Asset Management, Bloomberg, as of 30/03/2026

But inflation-linked bonds offer potential protection

Higher Inflation tends to weigh on conventional bonds, whose fixed nominal yields are not correlated to rising prices. While investors continue to receive the stated coupon, their real value is eroded as inflation picks up, compressing real returns.

Inflation-linked bonds in contrast enable investors to stay ahead of inflation because the cash flows paid out are adjusted to reflect the rise in prices. Inflation-linked bonds benefit from daily indexation to total inflation, including the food and energy components.

Principal and coupons grow over time thanks to this daily indexation process. As time passes, the principal increases at the same rate as the corresponding inflation rate.

The inflation indexation works gradually over time, meaning that in highly volatile environments, like those markets are currently experiencing, inflation linked bonds returns are mainly driven by movements in real interest rates.

But by focusing on short-dated inflation linked bonds (i.e. one-to-five year maturities) an investor can limit the impact of changes in real interest rates on returns and focus on the benefits of inflation indexation.

If you came for breakevens, stay for realised inflation

Short-dated inflation-linked bonds’ performance in March demonstrates their capacity to protect investors from an inflation shock. Inflation breakevens delivered +1.15% of performance and absolute performance of short-dated inflation linked bonds is +0.05% (month-to-date as of 30 March). This compares with the performance of -1.10% for short-dated nominal bonds (performance data is USD hedged).

We remain constructive on the outlook for short-dated inflation-linked bonds. In our view, inflation breakevens are currently perfectly pricing higher energy prices in the short term and therefore higher inflation for the rest of the year.

This means that for breakevens to rally further, we need to experience a further sustained increase in energy prices from current levels or any other shock on inflation (tariffs, supply chain disruptions, higher wages, etc.)

Such a shock could result from an unfavourable scenario, with persistence of very severe constraints on traffic through the Strait of Hormuz, keeping hydrocarbon – oil and gas -prices at very high levels - e.g. an average of US$100 per barrel in 2026, before falling back (to around $80) in 2027.

This scenario would imply persistent strains on European gas supplies, particularly during the pre-winter stock-building period; prices would reach around €70 per megawatt hour on average in 2026 and €61 per MWh in 2027. In addition, we could also consider second round effects from the strains in Hormuz coming from higher fertilizer prices (leading to higher food inflation) and the lower supply of byproducts of gas production like helium.

With what we see as a fair pricing of inflation expectations, we believe that the main source of performance for short-dated inflation-linked bonds increasingly relies on realised inflation: The recent energy shock and the consequent uplift in prices will translate into higher income coming from inflation indexation.

As seen in the chart below, under current market conditions, we estimate the income from short-dated inflation-linked bonds will be between 3% and 3.5% between April and year-end, driven primarily by the inflation indexation mechanism:

Exhibit 2: Estimated income from short duration, euro-hedged inflation-linked bonds in 2026

Source: BNP Paribas Asset Management, Datastream – For illustrative purposes only. As of 16/03/2025. Performance calculation = Real yield + real yield change x duration + Inflation indexation + currency hedging cost or benefit based on 1 month rolling FX swaps.

We believe the amount of inflation indexation in the future months will be high enough to provide protection against a material sell-off in real rates, as occurred in 2022, a period with some similarities to today’s environment: an inflationary shock and fears that central banks would be forced to tighten monetary policy.

Moving towards stagflation

The tension in the Middle East constitutes a major supply shock, pushing inflation risks higher just as growth momentum across advanced economies was starting to deteriorate. Activity indicators were already pointing to weakening demand and softer labour markets. As a result, the macroeconomic backdrop increasingly resembles a stagflationary mix of slowing growth and persistent inflation pressures.

In this context, we favour short-dated inflation-linked bonds, particularly in the eurozone. This segment has proved to provide efficient protection against higher realised inflation while limiting exposure to interest rate swings.

At the same, we believe they will benefit from potential repricing of overly hawkish policy expectations, becoming the most efficient hedge against a stagflationary macroeconomic mix.

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Australia Ltd (ABN 47 107 346 841 AFSL 273320) (“AXA IM Australia”) and is intended only for professional investors, sophisticated investors and wholesale clients as defined in the Corporations Act 2001 (Cth).

This publication is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Market commentary on the website has been prepared for general informational purposes by the authors, who are part of AXA Investment Managers. This market commentary reflects the views of the authors, and statements in it may differ from the views of others in BNP Paribas Asset Management.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk , including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested.