The Iran war: So, is it all over?

Is the Iran war over? The answer, at least as far as the markets are concerned, depends on which index you look at. To judge by the level of equity indices and credit spreads, the answer seems to be clearly “yes”.

As of the close on Thursday 16 April, the MSCI All Country World Index was 1% above where it stood on 27 February, before the recent conflict began. Spreads for most US and Europe investment grade and high yield credit indices are below pre-war levels (the exception is pan-European high yield). The US Dollar Index (DXY), which measures the dollar versus a basket of currencies, shows the greenback just 0.6% stronger than at the start of the war, down from its 3% peak.

Contrary indications come from oil prices, with Brent oil at $99 per barrel - still $28 above the end-February quote - and government bond yields, which have yet to return to pre-war levels: the 10-year US Treasury and German Bund yields are each still 35 basis points higher.

Our multi-asset team’s view is aligned with that of equity markets: we are overweight risk. We believe investors who have not yet unwound their risk-off positioning may potentially have an opportunity to do so at better prices as the situation in the Middle East is unlikely to evolve smoothly. The possibility of a breakdown in negotiations and a resumption of hostilities cannot be excluded.

Aligned value

The sell off on 30 March may mark the post-war low for equity markets, and since then, ‘value’ indices (Russell 1000 Value, MSCI Europe, MSCI Japan and emerging markets ex-technology) have performed similarly, with returns from 6.7% to 7.2% over the last two weeks. The narrow range of returns across these indices is not surprising, as that had been the case previously.

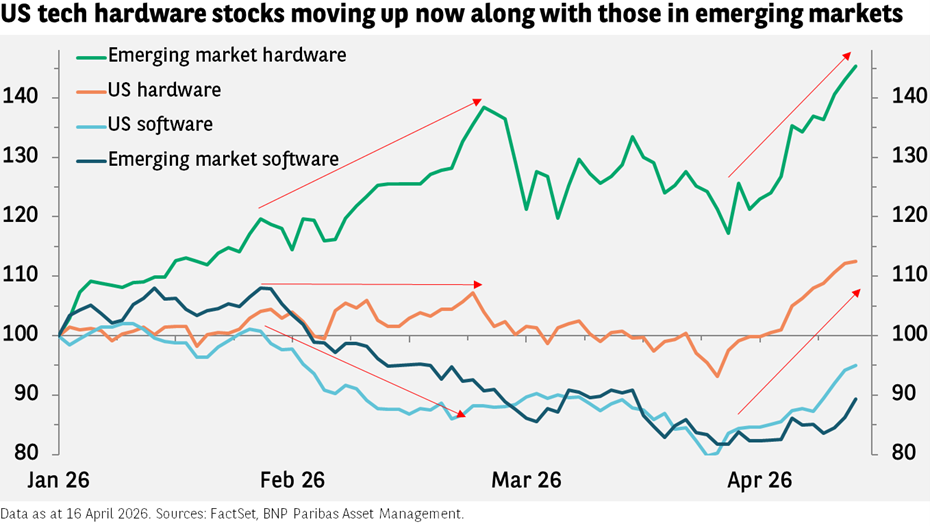

By contrast, the pattern of returns for US and emerging market hardware stocks has changed dramatically. During the first quarter earnings season, several tech companies announced plans to significantly increase their capital expenditures, which lead to a surge in the stocks of emerging market tech hardware and semiconductor companies - the primary beneficiaries of the largess.

US hardware stocks did not benefit. Coincidentally, new artificial intelligence tools spurred worries about the outlook for software stocks globally, and both US and EM stocks declined. However, all the indices have rallied over the last few weeks (see exhibit).

If the war continues to wane as a factor driving markets, the results of the impending Q2 earnings season should predominate. Don’t forget that another contributor to US tech stocks’ poor performance in the last quarter was disappointing results compared to high expectations.

Those expectations are arguably even higher this quarter, at least for emerging market hardware companies, thanks to the capex surge: earnings are forecast to more than double versus the same quarter a year ago. For the Nasdaq 100 index, the expected gain is only 23%. It remains to be seen how tolerant investors will be if growth fails to meet expectations, amid what are still likely to be potentially very strong results.

Data sources: FactSet, BNP Paribas Asset Management, as of 16 April 2026. Past performance should not be seen as a guide to future returns.

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Australia Ltd (ABN 47 107 346 841 AFSL 273320) (“AXA IM Australia”) and is intended only for professional investors, sophisticated investors and wholesale clients as defined in the Corporations Act 2001 (Cth).

This publication is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Market commentary on the website has been prepared for general informational purposes by the authors, who are part of AXA Investment Managers. This market commentary reflects the views of the authors, and statements in it may differ from the views of others in BNP Paribas Asset Management.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk , including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested.