Take Two: Global stocks endure fresh volatility; Eurozone inflation falls

What do you need to know?

Global stocks endured a fresh bout of volatility last week amid renewed uncertainty over US trade policy but were subsequently boosted by strong corporate earnings. The MSCI World NR Index rose 1% over the week to Thursday’s close*, while the UK’s FTSE 100, Euro Stoxx 600 and Japan’s Nikkei reached fresh record highs. Markets fell at the start of last week following US President Donald Trump’s announcement of fresh tariffs, after the US Supreme Court overruled some of the levies imposed in 2025. Global indices then recovered as the new tariffs came into effect at a lower rate than initially expected.

* In US dollar terms. Source: FactSet, data as of 26 February 2026

Around the world

Eurozone annual inflation fell to 1.7% in January, in line with the preliminary estimate and down from December’s 2.0%. The 16-month low reflected a fall in energy prices and a slowdown in services inflation. Core inflation, which excludes energy, food, alcohol and tobacco, edged down to 2.2% from 2.3%. Separately, Germany’s economy returned to growth in the fourth quarter of 2025, expanding by 0.3% on a quarterly basis after a flat reading in Q3. The rise was primarily driven by household and government spending.

Figure in focus: RMB 803.5 billion

Tourism spending in China reached a record RMB 803.5 billion (around US$117 billion), from some 596 million domestic trips taken during the Lunar New Year holiday in February. Both figures represent an almost 19% increase from the same period last year, according to Reuters. This year’s Spring Festival was extended from eight to nine days, in a government effort to boost consumer spending and encourage households to travel, shop and seek entertainment. However, spending per domestic trip fell slightly by 0.2%. The slight dip could suggest Chinese consumers remain cautious despite government stimulus.

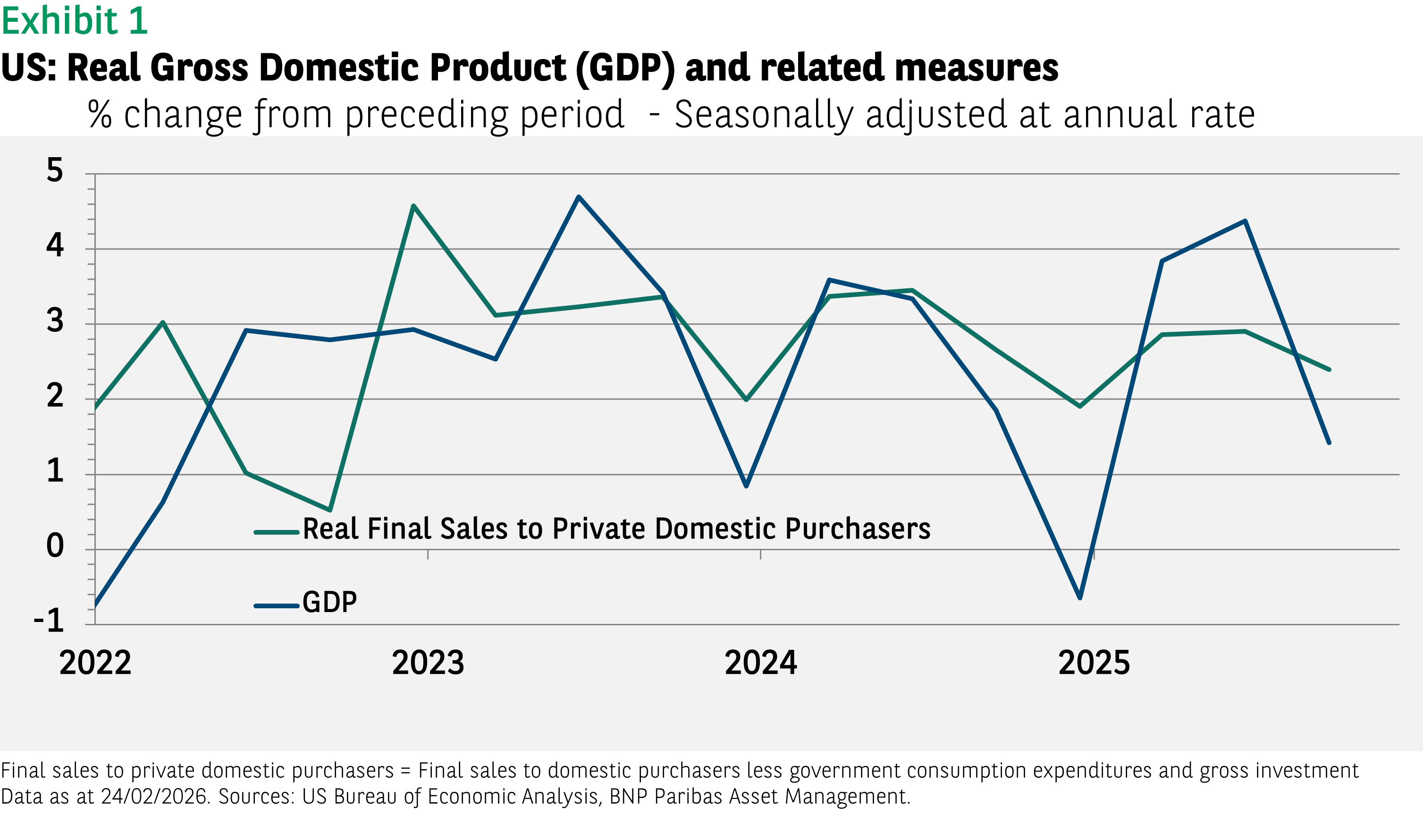

Chart of the week

Fourth quarter US GDP growth came in at 1.4% (seasonally adjusted annual rate), the recent advance estimate showed. It was both a slowdown from Q3’s 4.4% and disappointing versus consensus estimates. Nevertheless, the underlying data was more encouraging. First, there was a sizeable drag to quarterly GDP growth (-0.9 percentage points) from lower federal government consumption and spending, because of the partial government shutdown. Second, final sales to private domestic purchasers have been much less volatile than GDP. Private domestic demand (consumption plus investment) has been hovering around 2.5% for the past two years, underlining US growth’s resilience.

Words of wisdom

HALO Trade: Companies with tangible assets and a lower risk of disruption from technological change have garnered investor and media attention recently, amid concerns over artificial intelligence spending and threats to company business models. Those with heavy assets and low obsolescence – the so-called HALO trade – include companies in the commodities, infrastructure, logistics, and food sectors, among others. These are generally viewed as defensive sectors that could prove more resilient in periods of macroeconomic uncertainty. While technology and AI could potentially improve efficiency and productivity in such areas, the underlying assets themselves are unlikely to be replaced.

What’s coming up?

On Tuesday, the Eurozone issues a preliminary estimate of February’s inflation rate, and the UK government delivers its Spring Statement where it will outline its growth and spending expectations. Wednesday sees several final composite Purchasing Managers’ Indices released, including those covering Japan, China, the Eurozone, US and UK. China’s Two Sessions, its annual legislature and policy meetings, begin on Wednesday and will see the government announce its next five-year plan for economic growth. On Friday the Eurozone publishes the final estimate of its Q4 GDP growth rate, and the US updates the market with jobs data.

Read more insights at the Investment Institute

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Australia Ltd (ABN 47 107 346 841 AFSL 273320) (“AXA IM Australia”) and is intended only for professional investors, sophisticated investors and wholesale clients as defined in the Corporations Act 2001 (Cth).

This publication is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Market commentary on the website has been prepared for general informational purposes by the authors, who are part of AXA Investment Managers. This market commentary reflects the views of the authors, and statements in it may differ from the views of others in BNP Paribas Asset Management.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk , including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested.