Take Two: Markets reach fresh highs on peace hopes; and Eurozone business activity contracts

What do you need to know?

Global stock markets rallied last week amid investor optimism over a peace deal between the US and Iran, as well as strong corporate earnings from technology firms. Hopes of an end to the Middle East conflict prompted oil prices to retreat, easing inflation fears. Meanwhile strong demand for artificial-intelligence related stocks helped the MSCI World Index, the S&P 500, the tech-heavy Nasdaq and Japan’s Nikkei 225 reach fresh highs. The MSCI World Index and S&P 500 were each up 2% in the week to Thursday’s close while the Nasdaq rose 4% and the Nikkei gained 6%.*

*In US dollar terms. Source: FactSet, data as of 7 May 2026

Around the world

Eurozone business activity contracted for the first time in almost a year and a half, amid high energy prices due to the Iran war. The composite Purchasing Managers’ Index fell to 48.8 in April - a reading below 50 indicates contraction - from 50.7 in March, a 17-month low. A sharp decline in services offset higher manufacturing production as companies increased stock levels amid geopolitical uncertainty. Elsewhere, the US composite PMI rose to 51.7 in April from 50.3 the previous month, as services and manufacturing activity improved. China’s composite PMI rose to 53.1 from 51.5, while Japan’s composite PMI slipped to 52.2 from 53.0.

Figure in focus: 200 billion

Almost 200 billion cubic metres of natural gas could be made available annually if countries better tackle methane emissions and gas flaring, according to the International Energy Agency. Methane emissions from the energy sector neared record highs in 2025 despite international commitments to reduce levels in line with climate targets. However, tackling methane could help countries increase energy security. Efforts to cut methane from oil and gas operations globally could deliver nearly 100 billion cubic metres of gas to markets each year, while eliminating non-emergency gas flaring could unlock a further 100 bcm, the IEA said.

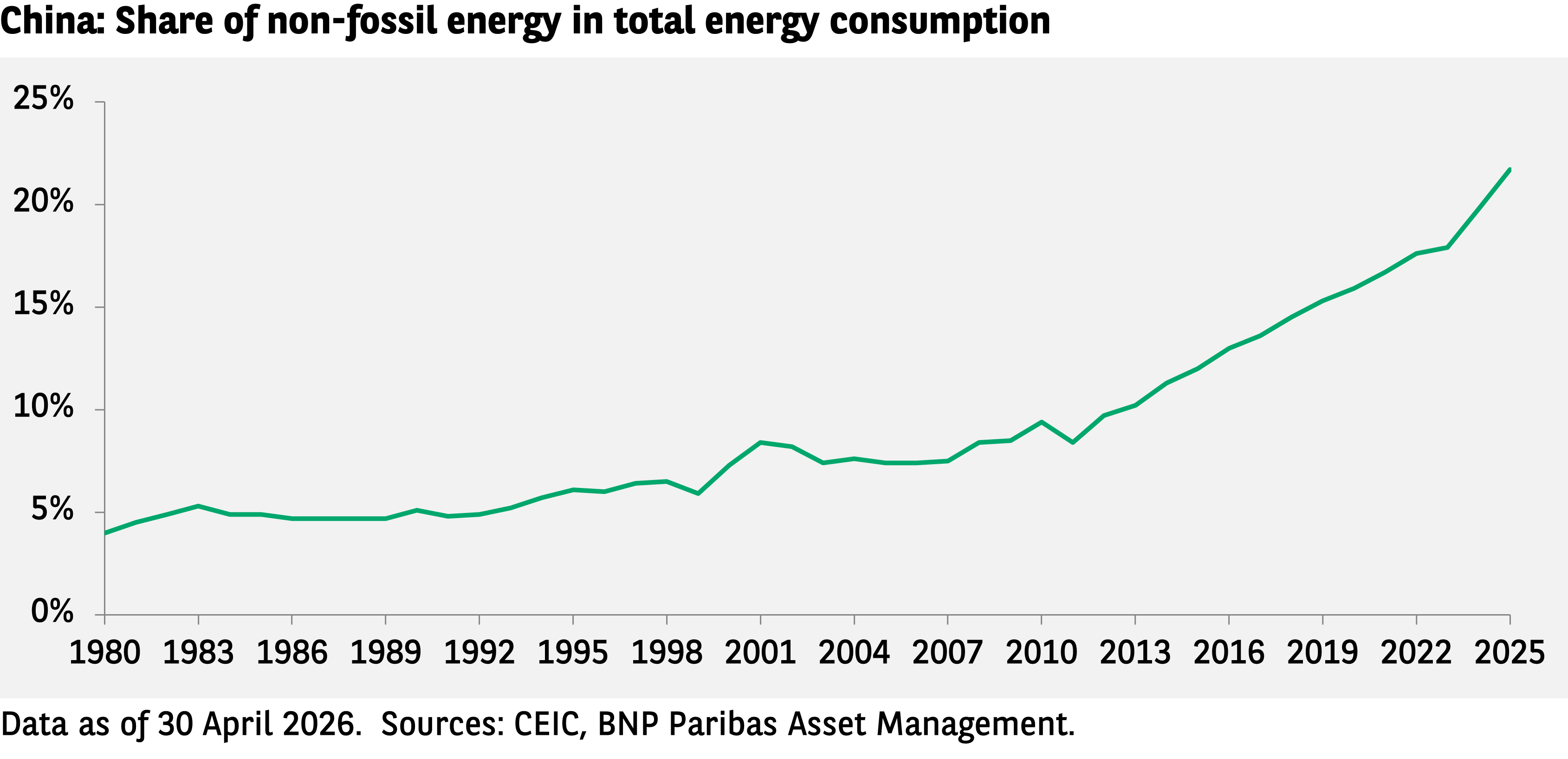

Chart of the week

The energy supply shock from the Middle East conflict seems to have had a moderate impact on China, partly because of China’s transition to non-fossil fuel energy consumption, which now accounts for 22% of its total. The energy transition effort is expected to intensify, with Beijing aiming to achieve peak carbon emissions by 2030 and carbon neutrality by 2060. Crucially, China’s 15th Five‑Year Plan, covering 2026-2030, targets lifting the share of non‑fossil fuels in the country’s total energy consumption to 25% by 2030, 30% by 2035, and 80% by 2060.

Words of wisdom

Megatsunami: An extremely large wave created by rocks, ice or other materials falling into the water below, that can occur following earthquakes and landslides. New scientific research has found a link between megatsunamis and climate change, after analysing a 2025 megatsunami in Alaska. Climate change was responsible for a large glacier moving and exposing a large mass of rock, which fell into a fjord creating an almost 500-metre high wave – the second tallest wave ever recorded. The risks of megatsunamis are increasing as glaciers continue to retreat at rapid rates, the scientists warned, but satellite and sensor data could help to predict them.

What’s coming up?

China updates markets with its latest inflation data on Monday. The US follows with its own inflation figures on Tuesday, while the Eurozone publishes its ZEW Economic Sentiment Index. Wednesday sees the Eurozone issue a second estimate of its first quarter GDP growth rate while the UK publishes a preliminary estimate of its own Q1 GDP growth on Thursday. On Friday, the US reports industrial and manufacturing production figures.

Read more insights at the Investment Institute

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of BNP PARIBAS ASSET MANAGEMENT Europe or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Australia Ltd (ABN 47 107 346 841 AFSL 273320) (“AXA IM Australia”) and is intended only for professional investors, sophisticated investors and wholesale clients as defined in the Corporations Act 2001 (Cth).

This publication is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Market commentary on the website has been prepared for general informational purposes by the authors, who are part of AXA Investment Managers. This market commentary reflects the views of the authors, and statements in it may differ from the views of others in BNP Paribas Asset Management.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk , including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested.