Take Two: IMF lowers global growth forecast

What do you need to know?

The International Monetary Fund lowered its 2026 global economic growth forecast to 3%, from April’s 3.1% projection. The modest downgrade reflects the ongoing impact of the Middle East conflict and trade fragmentation but is partly offset by advances in artificial intelligence. However, the IMF expects growth to rebound to 3.4% in 2027. Meanwhile it also anticipates that global headline inflation will rise to 4.7% in 2026 - an increase from 4.1% in 2025 - before easing to 3.9% in 2027.

Around the world

Federal Reserve officials were split over the future direction of monetary policy but expect inflation to remain elevated in the near term, minutes of their first meeting under new Chair Kevin Warsh showed. They voted to leave interest rates on hold at 3.5%-3.75% in June, reflecting concerns over upside inflation risks. However, some policymakers felt the Fed funds rate should be within or slightly below the current target range at the end of this year, while others thought it should be higher. “Participants noted that their future policy actions would depend on incoming information,” the minutes said.

Figure in focus: 1%

China annual inflation rose more slowly than expected in June as elevated energy costs continued to weigh on domestic demand. The consumer price index rose 1%, below market expectations of 1.1% and easing from May’s 1.2%. Core inflation, excluding more volatile food and energy prices, also rose 1% and down from 1.1% the month before. Separately, the World Bank forecast China’s economy will slow to 4.4% growth in 2026 and 4.3% in 2027 from 5.0% in 2025 amid continued weakness in domestic demand, a new report showed.

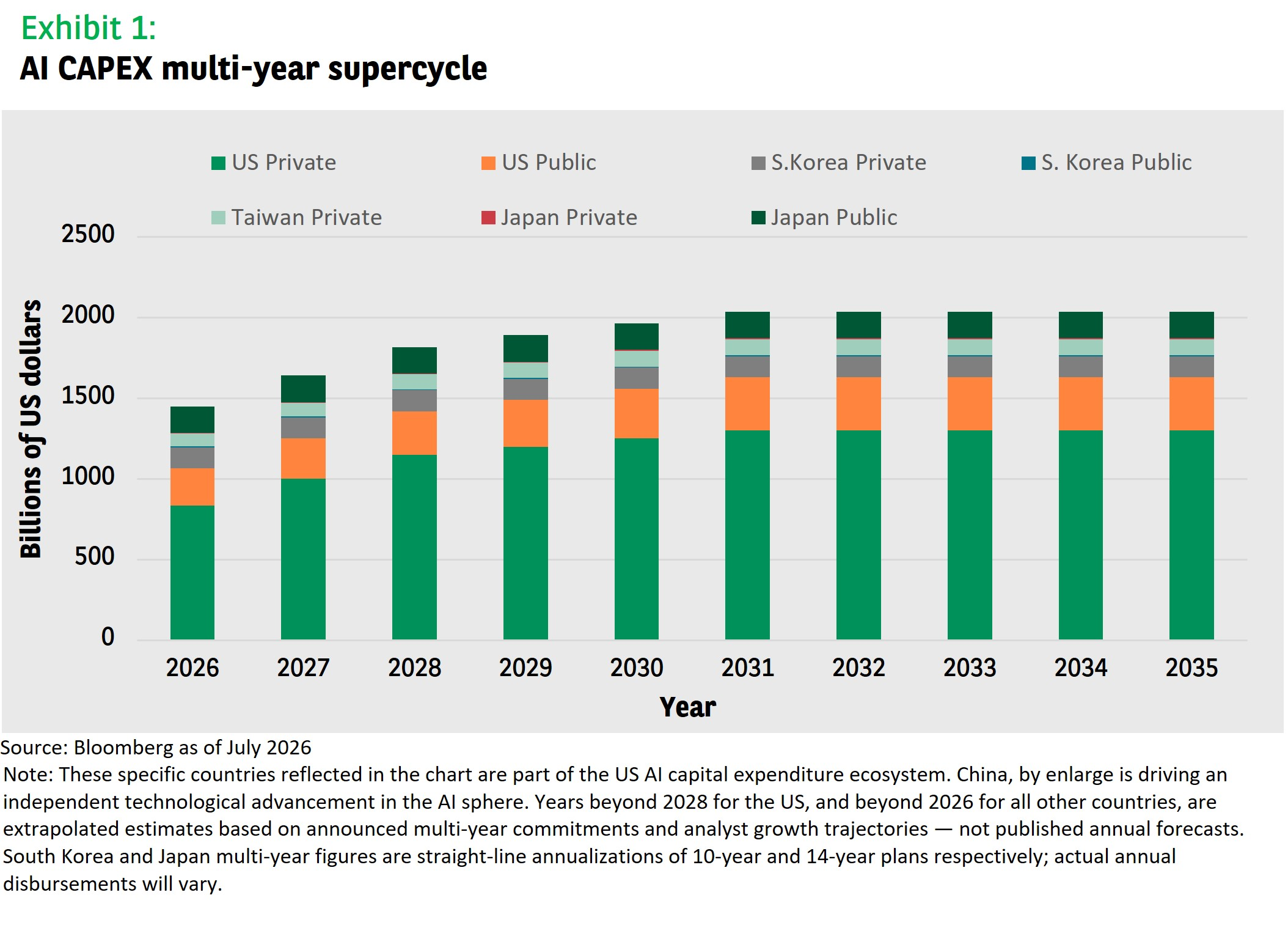

Chart of the week

Artificial intelligence capital expenditure in 2026 reflects an unprecedented concentration of investment across the US, South Korea, Taiwan and Japan, with an approximately $835 billion commitment from the top US hyperscalers alone. This underscores a structural shift in how technology and industrial policy intersect – governments and corporations are no longer treating AI infrastructure as discretionary, but as a strategic imperative. Korean conglomerates – part of the AI supply chains – are scaling investments to match the increased demand for compute capacity. Japan’s current administration recently announced a 14-year investment plan including an estimated $600 billion of support for AI and semiconductors. Collectively, these and other commitments suggest AI infrastructure investment is entering a multi-year supercycle that is poised to fuel growth.

Words of wisdom

Neoscaler: Neoscalers are smaller, regionally focused cloud providers specialising in high-performance infrastructure for artificial intelligence model development. Unlike so called hyperscalers, which provide services to organisations needing large-scale data processing and storage, neoscalers provide AI developers with more tailored model training capabilities and infrastructure. Neoscalers could provide a new challenge to hyperscaler dominance across the AI stack, according to a new report from consultancy Alvarez & Marsal.

What’s coming up?

On Tuesday the US publishes a flash inflation estimate for June – its annual rate increased to 4.2% in May. Wednesday sees China issue second quarter GDP growth figures, while the Bank of Canada convenes to decide on interest rates. On Thursday, the UK publishes its GDP growth rate for May. On Friday the Eurozone publishes a final estimate of June’s inflation rate – the most recent data came in at 2.8% for June, down from May’s 3.2%.

Read more insights at the Investment Institute

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Australia Ltd (ABN 47 107 346 841 AFSL 273320) (“AXA IM Australia”) and is intended only for professional investors, sophisticated investors and wholesale clients as defined in the Corporations Act 2001 (Cth).

This publication is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Market commentary on the website has been prepared for general informational purposes by the authors, who are part of AXA Investment Managers. This market commentary reflects the views of the authors, and statements in it may differ from the views of others in BNP Paribas Asset Management.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk , including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested.