Why ETF investors should not overlook active fixed income

KEY POINTS

Flows into European ETFs last year remained dominated by equity ETFs, but with record flows for 2023, fixed income ETFs are quickly gaining ground.

With investors increasingly seeking the opportunity to apply the potential benefits of an ETF vehicle beyond traditional indexed equity, there’s good reason to believe fixed income ETFs can maintain this momentum through 2024 and beyond. Of course, much of that will depend on the fixed income market environment.

Opportunities to put cash to work in fixed income

A substantial pool of liquidity, housed in money market funds looms over the financial markets. An examination of previous economic cycles indicates that this robust preference for liquidity is likely to diminish at some stage, particularly if the European economy steers clear of a severe recession and the European Central Bank (ECB) edges closer to rate cuts. Investor reallocations could unleash a flood of cash into risk assets.

Nonetheless, the timing of this shift and the specific asset classes that will benefit from it will hinge on several variables that are challenging to predict, such as the trajectory and pace of future ECB policy actions, persistent inflationary pressures, risks to economic expansion, and, notably, investor behaviour in the midst of uncertainty.

Our primary assessment is that cash seeking higher returns is likely to flow into shorter-term bonds, attracted by appealing yield levels and the potential for price appreciation as yields decline.

Why consider an active approach to fixed income ETF investing?

Fixed income is set to be a major priority for investors seeking to navigate a demanding market landscape in 2024. For those reassessing their fixed income allocations, utilising active fixed income management via an ETF structure offers investors diversification, liquidity, transparency and a cost-effective method for portfolio construction.

Furthermore, in the ETF space, the discussion surrounding active versus passive management becomes particularly prominent during periods of interest rate adjustments.

Active managers possess the capability to actively react to economic fluctuations and policy announcements, potentially maximising capital gains. In a volatile market, active bond management enables the portfolio manager to swiftly adjust their portfolio as economic indicators evolve and central banks alter their stance on interest rate policies. For example, sector allocation can be guided by the investment team's capacity to identify relative value opportunities within the investment universe, potentially creating significant value over time

Where in Fixed Income can ETF investors find opportunities?

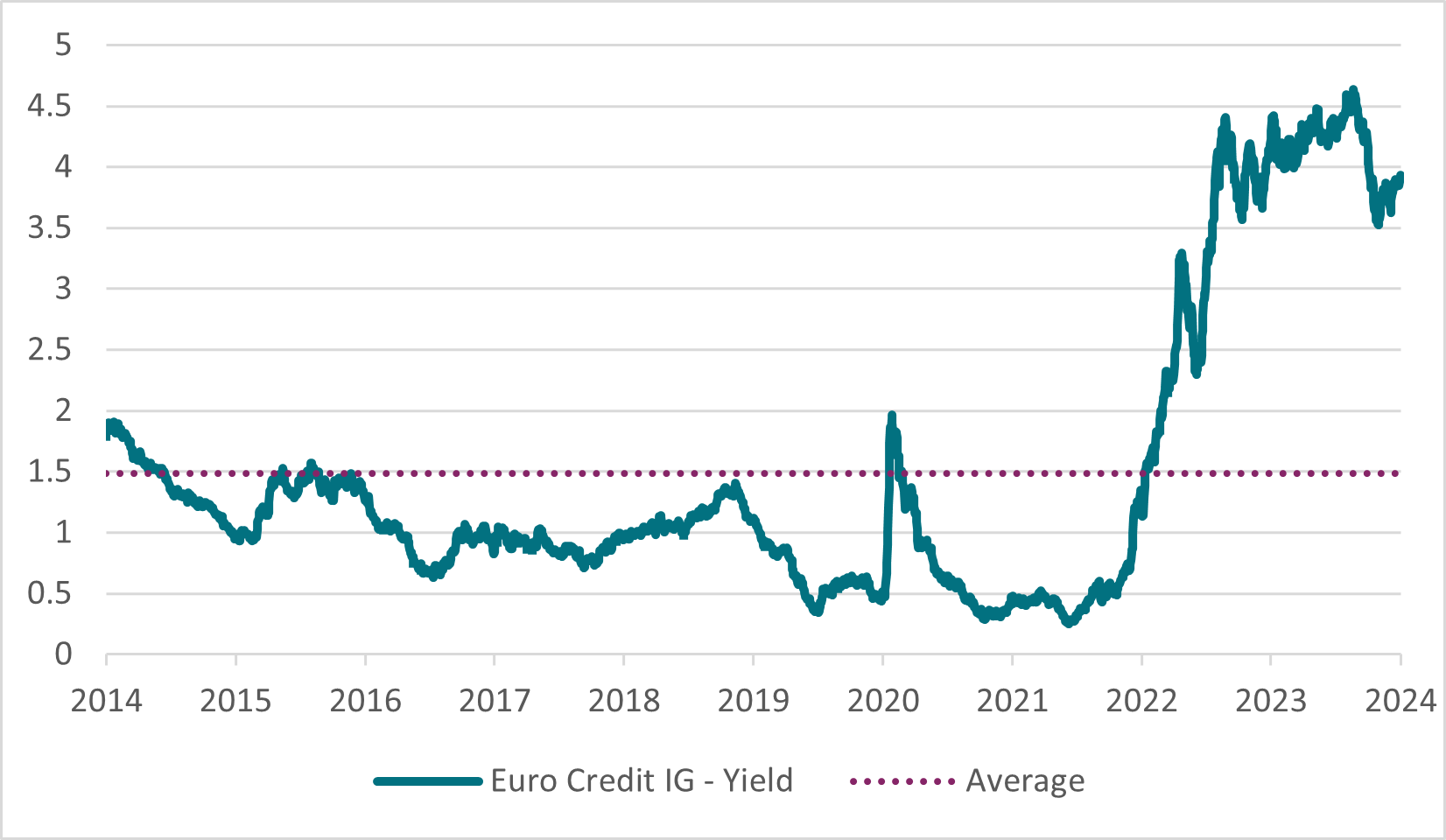

For ETF fixed income investors, European credit looks well-placed to offer opportunities in 2024. As the chart below shows, valuations continue to remain attractive as Euro Credit IG index delivers about 4% yield

Yield of Euro Credit IG index %

Source: AXA-IM, Bloomberg as of 29 February 2024

Second, fundamentals remain resilient and if there is a soft landing, we believe that the investment grade (IG) asset class should resist. We have seen some deceleration in trends since Q3 2023, and this deceleration will continue in the coming quarters. Finally, the yield attractiveness of the asset class has been a strong support for credit markets, resulting in significant inflows and the easy absorption of primary issuance in 2023. 2024 has already started on a positive footing with inflows accelerating in Euro Credit IG strategies, showing the attractiveness of credit markets over risk-free or low risk products.

Disclaimer

BNP Paribas Group's acquisition of AXA Investment Managers was completed on 1 July 2025, and AXA Investment Managers is now part of BNP Paribas Group.

This website is published by AXA Investment Managers Australia Ltd (ABN 47 107 346 841 AFSL 273320) (“AXA IM Australia”) and is intended only for professional investors, sophisticated investors and wholesale clients as defined in the Corporations Act 2001 (Cth).

This publication is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute on the part of BNP Paribas Asset Management or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Market commentary on the website has been prepared for general informational purposes by the authors, who are part of AXA Investment Managers. This market commentary reflects the views of the authors, and statements in it may differ from the views of others in BNP Paribas Asset Management.

Due to its simplification, this publication is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this publication is provided based on our state of knowledge at the time of creation of this publication. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

All investment involves risk , including the loss of capital. The value of investments and the income from them can fluctuate and investors may not get back the amount originally invested.